Estrazione Insights

| ID Insight | Titolo | Testo | Categoria |

|---|---|---|---|

| 74 | Monetise Assets | Lorem ipsum dolor sit amet, consectetur adipiscing elit. Curabitur vel malesuada augue. Suspendisse cursus pulvinar augue eget suscipit. In vulputate tortor in turpis malesuada porta. Curabitur pulvinar dolor ac ultrices volutpat. Aenean porttitor, mauris sit amet aliquet porttitor, arcu neque imperdiet lacus, ut porta tortor magna nec dui. Vestibulum ut ligula a risus suscipit faucibus. Ut facilisis ipsum a tellus consequat, vel aliquam lorem fermentum. Fusce gravida diam eget fermentum ultrices. Vestibulum eu aliquam libero, eget malesuada massa. Aliquam ac vehicula lorem, vitae consectetur lorem. Quisque in suscipit dui. Proin a risus lacinia, vulputate eros in, ullamcorper augue. Fusce molestie purus non magna mattis scelerisque. Praesent varius tristique tempor. Nulla sagittis diam vel ipsum hendrerit venenatis. Sed ultricies eget turpis eget pellentesque. Maecenas ullamcorper metus non tempus vulputate. Donec sollicitudin sem elit, vel feugiat quam ultricies quis. In varius enim eu vestibulum placerat. Class aptent taciti sociosqu ad litora torquent per conubia nostra, per inceptos himenaeos. Donec imperdiet porttitor libero eget posuere. Ut sit amet posuere arcu, non semper velit. Vestibulum lobortis nunc ut lorem auctor fringilla. Nullam vel fringilla eros. Donec cursus, lectus in tincidunt posuere, eros dui pretium massa, vitae egestas ipsum risus eget leo. | Blog |

| 76 | Engage Customers | Lorem ipsum dolor sit amet, consectetur adipiscing elit. Curabitur vel malesuada augue. Suspendisse cursus pulvinar augue eget suscipit. In vulputate tortor in turpis malesuada porta. Curabitur pulvinar dolor ac ultrices volutpat. Aenean porttitor, mauris sit amet aliquet porttitor, arcu neque imperdiet lacus, ut porta tortor magna nec dui. Vestibulum ut ligula a risus suscipit faucibus. Ut facilisis ipsum a tellus consequat, vel aliquam lorem fermentum. Fusce gravida diam eget fermentum ultrices. Vestibulum eu aliquam libero, eget malesuada massa. Aliquam ac vehicula lorem, vitae consectetur lorem. Quisque in suscipit dui. Proin a risus lacinia, vulputate eros in, ullamcorper augue. Fusce molestie purus non magna mattis scelerisque. Praesent varius tristique tempor. Nulla sagittis diam vel ipsum hendrerit venenatis. Sed ultricies eget turpis eget pellentesque. Maecenas ullamcorper metus non tempus vulputate. Donec sollicitudin sem elit, vel feugiat quam ultricies quis. In varius enim eu vestibulum placerat. Class aptent taciti sociosqu ad litora torquent per conubia nostra, per inceptos himenaeos. Donec imperdiet porttitor libero eget posuere. Ut sit amet posuere arcu, non semper velit. Vestibulum lobortis nunc ut lorem auctor fringilla. Nullam vel fringilla eros. Donec cursus, lectus in tincidunt posuere, eros dui pretium massa, vitae egestas ipsum risus eget leo. | Blog |

| 78 | Support Innovation | We live in a world that is more globalised than ever before. Making connections is now easy. Technology is to thank for this as we use it to support everyday activities from sending emails, calling friends, shopping at the supermarket, travelling on the tube and even buying coffee. Every one of these actions, and in fact everything we do, is generating data.Many companies have begun to realise that they already have a lot of data at their disposal, if only they knew how to utilise it. This dataset is only going to increase with research reporting that 90% of data in the world was created in the last three years. The growth of social media has contributed to this with businesses now having to monitor and react in real time to what is being said on channels including Twitter, LinkedIn, Facebook, Instagram and Google+. Companies can become true social businesses, by driving growth and superior profitability through a better understanding of the customer through social. They can capture, analyse and utilise these new forms of communication and data to drive real and measureable strategic value. Every industry from automotive to financial services and retail are sitting on masses of datasets relating to everything from machine data to customer behaviour. Data has significant potential as it provides an insight into human behaviour. Organisations are investing in business processes which depend on the accurate understanding of this data. They recognise that what was once regarded as ‘information overload’ can now provide valuable insights. When extracted correctly, data can help predict behaviours, classify profiles, decrease risk, identify opportunity, prevent fraud and can be used to discover meaningful patterns and trends. In fact, predictive analysis can help companies with customer service, compliance, financial management and making better informed business decisions. Now that we understand that big data has value in it, how do you go about finding it? Using big data intelligently involves more than just creating a huge database of internal and external business information. It requires adopting a new paradigm for production and service delivery, using methods of computational intelligence, machine learning and evolutionary programming within artificial intelligence. The global adoption of smart phones, tablets, wearables and the hype around the internet of things means that datasets that were once merely observed can now be combined with volunteered data (as we see on social media) and cross referenced against intelligent statistics. These datasets are then analysed further using artificial intelligence methodologies. | Blog |

| 80 | Rethink Your Business | Digital transformation is unstoppable. Digital is persistent, ubiquitous and affects every industry and business. This means that all organisations need to understand the impact digital will have on their products, services, systems, infrastructure and, critically, their business model and organisational structures.

Today, despite the level of disruption, digital is only in its early days as mobility, analytics and agility fundamentally change the relationship between companies and their customers. The world of tomorrow is about connections. Individuals will find themselves interacting with hundreds of M2M devices as they go about their daily lives. Everything from security cameras, home appliances, traffic sensors, healthcare devices, navigation systems, ticketing systems, payment systems and even vending machines. Financial services organisations need to consider what a successful company will look like in the future and how digital disruption can be exploited. Major companies mistakenly assume that they are being digitally disruptive when implementing new technology portfolios or using tools such as online platforms, social networking, predictive analytics and cloud. This is not enough. Using new technology does not automatically result in digital exploitation. First, you need to reimagine your business and meet the demands of customers living in a digital world. Then you need to predict behaviours. Digital innovation has given birth to a new customer journey. It is transforming the way people interact, transact, learn and handle their finances. Companies increasingly find themselves in a situation where the customer is in control. So much so, that customers are directing and designing their own customised experiences. The digital customer cares about four things; convenience, simplicity, speed and insight. Customers want 24/7 access to services, response to any queries in real time and meaningful dialogues with the brands they interact with, across multiple channels and interfaces. They demand hyper customisation and are increasingly in control. The Millennial population are a good example of individuals who from a young age have grown up using a smartphone and tablet. What started out a tool to make phone calls when out of the house or office, is now something much more as the millennial population intuitively make all their important decisions online. Mobility infrastructure has expanded and diffused to the point where almost everything is connected to a network. For Millennial customers, bank branches need to offer more than just financial advice for the visit to be worthwhile. Technology is also uncovering new un-banked and under-banked communities. Banks are now finding themselves focusing their efforts on retaining customers and building brand loyalty whilst also competing with traditional institutions, challenger banks and non-traditional players from sectors as diverse as transport (e.g. Uber), retail (e.g. Amazon) and technology (e.g. Apple, Google, Facebook). Financial services companies must respond to customer needs quickly or risk losing to these smarter entrants. | Blog |

| 83 | OLD CFO and CRO functions to converge as market volatility increases pressure on Banks | CFOs and CROs in the financial sector are facing a period of simultaneous and disruptive events consequent to the recent financial crisis. Markets and economic volatility together with regulatory and commercial pressures are producing a challenging environment never seen in the past. Finance and risk functions within many financial firms have begun to build a closer partnership and a greater coordination, impelled by a combination of factors including cost and effectiveness pressures, regulatory demands, a desire to do more stress testing, reports on credit and market exposures with the goal to provide faster and more accurate figures to support the top management strategic and operational decision processes. In this way finance and risk are different faces of the same coin and, though the two functions must remain separated, a closer collaboration is required to give different perspectives and vigorous debate to providing the CEO and Board with a balanced view. Following areas should be the first testing ground to promote joint activities between finance and risk, while assuring their independence:

Some key issues should be addressed in order to reach an effective risk-finance collaboration:

Be Team has already started to support its Clients to be successful in this emerging trend. Quantitative skills in designing measures and reporting on the banking and trading book, culture in data quality and knowledge of processes developed in the CFO area and data governance projects can be easily extended with few risk management skills to support an effective CFO CRO Convergence. | Blog |

| 85 | CFO And CRO Functions To Converge As Market Volatility Encreases Pressure On Banks | CFOs and CROs in the financial sector are facing a period of simultaneous and disruptive events consequent to the recent financial crisis. Markets and economic volatility together with regulatory and commercial pressures are producing a challenging environment never seen in the past. Finance and risk functions within many financial firms have begun to build a closer partnership and a greater coordination, impelled by a combination of factors including cost and effectiveness pressures, regulatory demands, a desire to do more stress testing, reports on credit and market exposures with the goal to provide faster and more accurate figures to support the top management strategic and operational decision processes. In this way finance and risk are different faces of the same coin and, though the two functions must remain separated, a closer collaboration is required to give different perspectives and vigorous debate to providing the CEO and Board with a balanced view. Following areas should be the first testing ground to promote joint activities between finance and risk, while assuring their independence:

Some key issues should be addressed in order to reach an effective risk-finance collaboration:

Be has already started to support its Clients to be successful in this emerging trend. Quantitative skills in designing measures and reporting on the banking and trading book, culture in data quality and knowledge of processes developed in the CFO area and data governance projects can be easily extended with few risk management skills to support an effective CFO CRO Convergence. | Homepage, Insights, Risk &. Compliance |

| 86 | Foreign Exchange Is A key Profit Area For Our Clients Where Automation And Innovation Are Now A “Must” | The FX market volume – the market where currencies are traded – exceeds 5tn dollars a day, making it the biggest and most liquid financial market globally. The FX catalogue include cash products (spot, forward, swap, ndf) and derivatives (options, structured products). The FX market is the backbone of international trade and global investing: on the one hand, it allows the sustainability of import and export whereas, on the other, forex is an asset class that allows to take benefit from international diversification both to buy and sell foreign assets and securities or currencies directly. Forex rates also form the basis for performance evaluation and risk management as they are used for hedging purposes against currency fluctuations to manage risk or used to speculate assuming risk betting on earning a return. Currencies are traded electronically and bilaterally over the counter: a must for a dealer is to be always connected globally to identify “where the market is”. The lack of transparency and the massive volumes of transactions that describe the FX markets entitled the development of specific mechanism to identify the rate to apply: a sort of benchmark called “fix” that is a single rate that reflects the value of one currency relative to others at a particular point in time, typically created from a snapshot of actual trades (unlike Libor that relies on estimated rates). A recent regulatory spotlight on alleged market rigging has accelerated a longstanding move to automated trading platforms: word wide regulators and organizations are working on proposals for changing financial benchmarks as well as data providers. Banks, fearing a move towards exchanges as it would further reduce margins and the value of costly investments into their own trading platforms, are stepping up to move away from traditional voice trading that are at the center of the probes. Those concerns are reinforced by the fact that the Regulatory bodies are aiming to introduce transparency mechanisms, timely confirmation of deals, pre/post trade disclosures to clients and clearing obligations with the scope of forcefully making over the market operations subject to control. As for the fix income and commodities products in the late 1990s, the change from voice to electronic in FX will be driven from a buy side reform: the adoption of transparent algorithms and the access to different size order, simply show a better alternative to traditional channels. In addition the electronic platforms enable a real global dimension to the FX business (resolving simple barriers like time zone constraints) allowing players to grant access to all emergent markets and meeting retail investor’s appetite. Across all products, electronic trading volume moved from single-digits in the early 2000s to 74 per cent last year (according to Greenwich Associates, a research company), but about 35 per cent of volume in the global $2tn a day spot fx market – where currencies directly change hands and traders take risks as market makers – is still done over the phone (according to Bank for International Settlements data): the rise of machine-driven fx business is open. Our experience on FX programme at one of our largest clients. Since 2011, one of our largest clients launched a wide program including initiatives to develop capabilities and technological assets on FX, enabling itself to expand its positions in currency trading, including:

Particular attention has been given to small/mid corporate and retail clients, developing a specific electronic platform integrated with the payment current services offered: the aim is to create synergies with all new potential FX transactions arising from products like structured export finance, trade export finance and cash pooling and to leverage its consolidated skills and competences on securities brokerage platforms (Market Hub). This is the vision our client has on electronic assets:

There is a clear picture described in the strategic business plan of our client: forex asset class has been recognized among the main profitable business for the next three years and the Group’s investment bank has been appointed as director to develop services and product to distribute a Group level. Be Consulting has been confirmed as partner to support this new challenge. | Market & Investment Banking |

| 405 | Mobile Payment: The New Frontier Of Mobile Banking | Banks that are focused on service level and innovation have grasped that m-banking is the hint to manage all the aspects of their customers daily lives, providing access to financial services through mobile devices. Mobile Payment represents a significant opportunity for Banks to create new revenue streams, being a centerpiece of a multi-channel strategy. Different actors have shown interest to aggressively enter this new market, but there is still no evidence of the sharpest way to move forward. In order to maintain their competitive advantage against new Players, Banks should leverage on their experience in dealing with security and data protection issues and exploit the value of mobility for customers (ubiquity, ease of use, convergence). Given Italian terrific penetration of cellular phones, m-Payment results in a great opportunity to attain the “War on Cash”, reducing cash related costs and enforcing Anti Money Laundering norms. There is an already settled demand for different m-payment use cases:

Next step in the evolution path will be the introduction of M-Wallet, enabling a real convergence of multiple offers on a single device: loyalty cards, m-payments, couponing and geo-positioning offers. The key market challenge is to redeem the conflict between Finance and TelCo’s players. Banks see in the m-payment an extremely valuable source of information on customers spending patterns and preferences, while MNO’s are starving for new data targeting and incremental advertising revenues. The m-Payment market appears to be wide open to new entrants, with banks having a slight edge. To survive in this market Banks have to integrate mobile into existing offerings and rebuild loyalty engagement strategy,based on geosensitive and profiled push communications At the same time Banks should truly address the market adoption of a NFC standard based on a micro-SD architecture, that’s allows them to counterbalance the overpowering strategy of new comers: Apple, Google, Paypal, TelCo’s and to catch new market opportunities deriving from:

A “wait and see” approach will let emerging providers peel consumers away from their banks. In this worst scenario Financial institutions will not only vanish m-payment new revenues opportunities, but will also suffer significant losses of current business. | Cards & Loyalty |

| 407 | Use Of Co-Browsing Technologies Pushes The Growth Of Remote Advice | Whilst the wealth management industry has been struggling with market volatility, low returns and increasingly risk averse clients, another phenomenon has been gradually gathering momentum. The incredible rise in ownership of smartphones such as Apple iPhone and Samsung Galaxy, plus plunging data tariffs and increasing broadband and Wi-Fi penetration has changed the way that people expect to be able to access and receive information. Many wealth managers have the view that the more a person is worth, the more face to face time they require. However, many of their clients priorities are different. They ask for more and better data, 24 x 7 access to portfolio positions, execution only trading with expert advice delivered not necessarily face to face, but at the clients desired time and place. The role of the Relationship Manager is under pressure, they are a costly resource but their role is no longer absolutely clear. Many clients are increasingly mobile and time poor. Therefore, they have become unwilling or unable to conduct all of their business face to face with a Relationship Manager. These evolving needs have resulted in an increased use of telephone and e-mail, neither of which however can deliver the richness of a person to person advice session. Some organisations have attempted to replace the face to face with video conferencing, but for anyone who has spent any time on Skype, the results can be very patchy. It may be fine for talking to relations, but not satisfactory for delivering complex investment advice! One solution to this dilemma is starting to get traction, the use of co-browsing technology. The concept is simple: a regular telephone call is made but both parties are also online looking at an internet browser. The advisor can “push” information to the clients’ browser, so that the client can see what the advisor is speaking about. All the client needs is a telephone, a laptop, tablet or PC and an internet connection. Suddenly complex investment products can be illustrated and explained with diagrams, illustration or even video. Documents can be securely and instantly delivered and agreement to compliance questions and statements can be remotely recorded. On the client side, these sessions can be conducted at a time and place to suit their needs but, at the same time, they get a much richer discussion than a simple telephone call or e-mail could deliver. This is certainly not a complete substitute for face to face, but where an existing relationship exists, or where time or geography are challenging, this type of meeting can have many advantages over a simple call or a complex video meeting. So far, where this technology has been deployed the advisors have experienced significant uplift in conversion rates on product sales, shorter sales cycles and reported higher levels of customer satisfaction. Because the entire conversation plus supporting documentation can be recorded in a visual audit, the numbers of complaints and miss-selling allegations has plummeted. In addition the advisors are able to deliver these sessions from their office and so save considerable time and cost on travel. There is no doubt that in the longer term, video conferencing will replace much of the need for travel and face to face meeting, however in the short term, and in particular in parts of the world where local infrastructure and internet access is limited, co-browsing technology can deliver a cost effective and rich alternative to a face to face meeting. | Homepage, Insights, Retail & Corporate Banking |

| 414 | Italian Prepaid Card Market: Any Room For Growth? | With 25 million prepaid cards issued, Italy is the largest prepaid country in the world. It is seen by many as a case study of what can be achieved by prepaid cards and a laboratory for new successful products. Unlike in other regions, where prepaid cards are used by a small proportion of under banked consumers, in Italy these are truly mass-market payment tools. Prepaid cards success in Italy is due to several reasons:

In Italy the majority of prepaid cards are issued by retail banks as general purpose cards, not targeted at specific consumer segments. Things are changing though: a growing number of non-banking institutions and service providers are looking towards the prepaid card market as a way to introduce innovative services and gain traction in the payments arena. Reflecting country’s preference for cash, prepaid cards are used mainly occasionally, for online purchases or as travels pocket. Hence the total value of transactions still remains limited. Given the record high penetration rate of prepaid cards, financial players face the challenge to increase cards’ utilization rate and move customers from plain vanilla prepaid cards to richer and more engaging products. Light accounts are a big step in the right direction: different pricing and additional services enabled by IBAN code allow for everyday usage and higher revenues. The market is already crowded, but new important products, such as Postepay Evolution from Poste Italiane, continue to emerge. What is next? Innovative features will become a requirement for new successful products:

We believe the prepaid space will stay as a profitable entry level for retail banks in the next years; increasing synergies between prepaid cards and smartphone applications will also ease the transition towards the approaching proximity mobile payments revolution. | Cards & Loyalty, Insights |

| 418 | Banks Need An “Holistic” Approach To Set Up Outsourcing Supervision And Monitoring Systems | Many European financial players are thinking of outsourcing large components of their operational and ICT services, as a consequence of a widespread trend to “focus on core business”. This strategy needs the implementation of an “outsourcing supervision and monitoring system”. This topic is subject to specific domestic and EU provisions which underline its growing importance in the broader context of the so-called “responsibility discipline” of financial players. New regulations, combined with the increasing managerial need of supervision and monitoring for the performance of the “operating machine”, led Be Consulting to develop a flexible and scalable “holistic” approach to the Outsourcing Management topic. It is a six-step approach:

| IT & Operating Model |

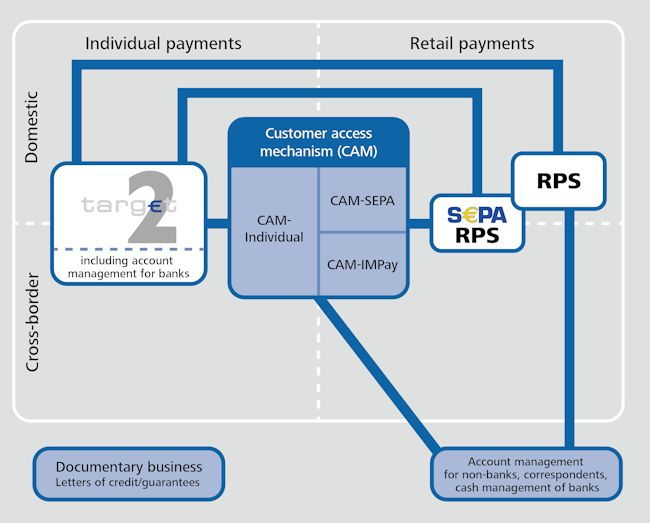

| 421 | The Impact Of T2S Is About To Reshape Securities And Payments Industries In Europe | The financial crisis of the first years of the new millennium pushed national and international financial and monetary Authorities to re-think the payments and securities settlement context. With reference to the Eurozone, the ECB decided to evolve the security settlement landscape by adopting the same approach they had followed for wholesale payments with the introduction of “TARGET 2”. In other words, to build a single shared technical settlement platform managed at centralised level and offered to Central Securities Depositories (CSDs). TARGET2-Securities (better known as T2S) is exactly that: a single shared platform, owned and operated by the Eurosystem, that has been offered to all CSDs interested to adopt it on a voluntary basis. At the moment, 23 CSDs have already expressed their commitment to adopt the new platform by by February 2017. “Early birds” – including the Italian CSD Montetitoli (part of the London Stock Exchange Group) – will go live on T2S on 22 June 2015. T2S is probably the largest project ever launched by the European Central Bank (ECB) in terms of resources and efforts. The rationale behind this tremendous effort relies on the fact that settlement is a critical process of systemic importance: it performs the closing of any securities deal as it allows the technical exchange of securities against cash, mainly in central bank money. For this reason, national securities settlement systems are (usually) considered as part of respective domestic payment systems. T2S is part of a bigger picture aiming to build a single European payment system including retail payments (via SEPA), wholesale payments (via TARGET 2) and collateral management issues (via the Collateral Central Banking Model, also known as CCBM). Jean-Michel Godeffroy, chairman of the T2S Programme Board stated that “the ultimate objective of T2S can be summarised in just a few words: to make Europe a better place to invest” (T2S OnLine – Quarterly review – No 11, Winter 2012). The involvement of the Eurosystem in building T2S and the sponsorship of all European Authorities, including the EU Commission, has generated large expectations around the project. Among others, it is expected that T2S will contribute to:

But expectations are never for free: if there were no doubts that the introduction of T2S mainly impacts on national CSDs that decided to join it, there is now a general consensus on the fact that T2S will affect the current market positioning of all intermediaries currently operating in the Eurozone, i.e. global custodians but also local agents, Central Counterparties (CCPs), trading venues and asset managers. In order to remain competitive they should all take critical decisions as if stay or not in the securities business and, if yes, how to comply with the new business framework. In brief, they should assess their current business model in relation to the new scenario and, if necessary, think about adopting a brand new one. Furthermore, the impact of T2S on the organization, the operations and the IT structures of all those securities industry actors will be significant. It was said that T2S will break up the current CSD monopoly at domestic level by “separating the ‘infrastructure’ from the ‘service’” (Ben Weller, June 2012). This was often (mis)interpreted as a commoditisation of the settlement services that will lead CSD to find new sources of revenues with higher margins: those services generally offered by Global and Local Custodians. The extent to which CSDs will succeed in offering other services, eminently banking, depend not only on legislation that will be introduced with the CSD Regulation but primarily on the reaction of those players whose business will be attacked by CSDs. CSDs will have to find a trade-off between:

or

Some of today’s most competitive CSDs at domestic level risk to get a worse market positioning as T2S will lead to an increase in their operating unit and to a greater competitive pressure on securities settlement fees. As for CSDs, T2S represents a mix of opportunities and threats for Global Custodians. The few large operators that can be considered as truly global (i.e. those that act directly in any, single, financial center with their own organization) will probably plan, in the long term, to rationalise the number of CSDs they work with. In the short term, they would probably decide not to change the current business model based on direct membership. As the majority of them work through local entities that offer them agency services, they will be geared to reduce the number of current local providers; this solution will imply that they have to plan additional costs to insource skills and know-how. T2S could have significant implications also for the sub-custodians (ie. the smaller local operators which normally act as local agent for global custodians). Even for them it could be necessary to rethink / refine their business model in order to keep the current competitive position. This will imply new investments and their operating costs will rise in the medium term. In addition, not all sub-custodians will be able to cope with the new challenge: they are fully aware about this issue that explains why an high percentage of sub-custodians expressed a negative opinion on T2S. The fragmentation of European markets was, in fact, the key to their success so far. Concerns also arise from the fact that there is a significant probability that the national CSDs in T2S may extend their operating scope to local custody services (in particular in the field of management of corporate actions, taxation, etc.). This event would hardly be counteracted by the local custodians, who would lose not only revenue but also their raison d’être. In fact, there would be space for only few operators who can aspire to the role of single point of access to a country involved by T2S and the ideal candidate is surely represented by the national CSD. The most likely consequence is, in the medium term, a consolidation of local operators or their conversion to the role of traditional commercial banks. CCP will play a key role in the post-T2S. Indeed, there are many clues to substantiate this statement. The new rules on OTC derivatives, the giving up to CCBM2 project, the increasing centrality of the role of collateral and – last but not least – the need to balance any negative network externalities, will make CCPs to become the key players in the development of the securities industry, even more than in the past. As the eminently domestic character of CCPs will lose importance progressively, only those structures able to support the growing demand for more sophisticated services, characterized by an international footprint , will survive. The others would probably be subject to mergers or acquisitions. The increased international competitiveness, together with the improved interoperability induced by T2S, could “crowd out” also those very efficient structures which, in terms of size, number of non-domestic participants and range of served asset classes, would be perceived as less “appealing”. Also companies who manage trading platforms will not remain indifferent to the advent of T2S. An easier access to standardised settlement services and harmonised custody services will blow traditional domestic boundaries, opening to greater contestability of the trading business and, ultimately, to an increase in competition. The use of a plurality of interoperable CCPs, the level of specialization on one or more asset classes, the range of products offered and the level of sophistication of the same, the ability to adapt to a more international context – characterized by a greater dynamics / responsiveness – are only some of the potential variables to be considered. T2S will probably not have a direct impact on trading platforms management companies in terms of operating costs or trading fees. More likely, it will push for an increase of competition between those companies. In conclusion, if for someone T2S can pose a threat to its competitive position, for someone else it could represent a source of new opportunities: “At the moment, the buzzword in the market is “collateral”. We are seeing considerable growth in secured borrowing. Also the future legislation on CCPs and OTC derivatives (EMIR) will require more margining. All regulatory initiatives point to the greater demands for more high-quality collateralT2S will enable banks to make very significant savings in collateral when settling securities transactions. T2S will eliminate the need for banks to hold multiple buffers of collateral in depository systems across Europe. Banks will have the possibility to have a single buffer based on their entire European business. A single pool of assets and liquidity automatically nets the short and long positions between various countries. A single settlement engine, central bank auto-collateralisation, a harmonised schedule, and many other features of the T2S platform, will also enable banks to reduce the amount of collateral that is left idle.”(Gertrude Tumpel-Gugerell’s keynote speech at the ECB’s conference on “Securities settlement in 2020: T2S and beyond”, Frankfurt, 4 October 2011). The recent financial crisis has exacerbated the relation between efficient management of collateral and its impact on capital adequacy needs of European banks. Following completion of a capital exercise, the European Banking Authority (EBA) determined in 2011 that the aggregated shortfall – corresponding to a minimum Core Tier 1 ratio at 9% – exceeds over € 100 billion. Under the pressure of the new market discipline agreed at G20 level to mitigate and – to a certain extent – prevent any new financial and monetary crises of systemic impact at global level, retail and wholesale payment systems will necessarily evolve and unsecured interbank deposit markets would be gradually replaced by guaranteed ones. Collateral is more and more a precious resource as it is more and more scarce: the current way of managing collateral shows some inefficiencies both internal (i.e. related to the specific business model of each market actor) and external (i.e. determined by the fragmentation of markets and platforms). These inefficiencies are estimated at about € 4 billion per year, of which about 10% originating from processes of over-collateralisation. Financial institutions aiming to keep their competitive positions in the new scenario will have to define strategies for integrating cash and securities in order to optimize risk and profitability management. Banks will look for more efficient collateral- and risk- management tools that, being integrated with payment and compliance processes, are able to work in a proactive way instead of simply reacting to market inputs. | Homepage, Insights, Transaction Banking & Securities |

| 493 | New financial products for the Italian SME Market | In the last few years, the ongoing Italian recession has had a significant impact on the Mid Corporate Market. Based on the latest Cerved data (i.e. an official Italian repository for Companies Balance Sheets) published in a report by the Bank of Italy, only 50% of companies have recovered their pre-crisis turnover. Moreover, companies have experienced a significant reduction of margins and profit, impacted by higher cost of credit (financial charge at 23% of EBITDA, +3% vs. previous year) and less fixed costs reductions. In this difficult economic scenario, there has also been a significant drop in investments. The request for financing has increased, mainly for short term products, driven by the increase in duration of commercial credit collection (avg. at 104 days, +10% vs. previous year). Given this challenging context, “Monti’s Technical Government” drafted several proceedings (collected in the “Decreto Sviluppo” document) to support the Italian economy. Among these, with particular reference to Article 32, are the new financial instruments designed to support the Italian SME market (Companies with turnover <50€m). These instruments, called “cambiali finanziarie” (finance bills) and “mini bond” can be issued by SME that are not listed if assisted by a financial sponsor (e.g. Banks, Investment Banks or Funds). These new financing products (or rather the evolution of the existing ones adapted for SMEs) can be issued by companies to raise short and mid-term financing (from 1 up to 36 months), creating new opportunities for both companies and Banks. This can be considered an important innovation if compared to the traditional SME financing approach, where the issuance of bonds was only possible for companies rated by an official Credit Agent. The effect of this old rule was to exclude SMEs from this market by definition. With the introduction of the sponsor role, the “Decreto Sviluppo”, opens the door for SMEs to a new and alternative form of financing. In this new scenario, banks can capitalize on new business opportunities and are set to play a centric role, firstly as a sponsor for specific SMEs and secondly as an investor in the Italian industrial sector. As a matter of fact, with this new regulation, banks will be obliged to keep within their portfolio part of the securities which will be issued and distributed primarily to other financial institutions. Be believes that there is a considerable business opportunity for us in providing a broader support to banks as they approach this new market. For example, in the Commercial area, Be can provide market analysis and sizing, revenue pool estimation as well as identify the risk of cannibalization for their existing product portfolio. In the Product and Operations areas, Be can support product and process design. On the latter, we are already in discussions with the Italian arm of one of the largest European banking groups, to define the scope of our assistance to the launch of cambiali finanziarie and mini bonds, through an “end-to-end” support (e.g. compliance, legal, booking, accounting). Be believes that helping Banks to provide these two new forms of financing is set to be a very important area of development for our Company, which also includes an element of “social responsibility” as it represents a concrete support to Italian Economy. | Insights |

| 496 | Cib Divisions Need To Launch New Product For SMEs | The financial crisis is bringing deep repercussions for the SME sector (small and medium enterprises) resulting in shrinking revenues with reduced strategic vision and low investment capability. This challenge is common across the EU region, but Italy, given the weight of its SME sector (>95% of total companies) is significantly under pressure. The primary effect of the crisis is the weakening of the balance sheet for SME companies and the subsequent difficulty in accessing credit via traditional bank lending products. In this difficult scenario, new alternative financing forms are being developed which allow SME’s to evolve their relationship with banks and buyers, leveraging the whole supply chain to gain easier and cheaper access to credit. Be has been engaged by a leading European bank to support the strategy definition of a new Supply Chain Finance offer for Corporate Banking, which will put us in a favorable position should the offer be implemented. Supply Chain Finance is a set of services (financial and non) that allows suppliers and buyers to manage the whole production and distribution chain, reducing financial costs and increasing the efficiency from origination to destination of goods exchanged. The key competitive advantage deriving from the SCF (the aforementioned set of products) is that is enables SME’s which supply a Large Corporate to finance their own working capital at a significant discount as, they can benefit from the credit rating of the Buyer. At the same time, Buyers are able to negotiate a better price for goods with their suppliers. The relationship between Buyer and Seller is strengthened by an SCF solution, encouraging both companies to prepare a common, mid-long term plan. Banks are increasingly entering this market, which is growing 30% y-o-y. Although they appear to lose revenues by providing loans at lower price, they grow overall revenues through new customer acquisition not otherwise achievable due to restrictions in terms of Risk Appetite. The Banks also grow margins by reducing the cost of risk (impairment) thanks to the better quality of their SME portfolio. SCF is therefore a win-win product, where Buyer, Seller and Banks all benefit from an innovative way to exchange new information (strategy, production plans, commercial targets) progressing from using only “old” balance sheet information to access finance. | Insights, Retail & Corporate Banking |

| 501 | In-Depth Investigations Can help Banks Preventing Frauds On Public Funds Allocation | Public funds attract an enormous number of organizations across Europe. Indeed, considering the overall amount of the funds and their relevance as tools for speeding economic growth and innovation, there is an increased attention from institutions and citizens to prevent this specific type of frauds. At EU level, OLAF (the European Anti-Fraud Office), has reported for 2012 and 2013 the opening of more investigations than in the preceding years (431 vs 253). However, also at national level, the fight against this type of frauds is progressing. In Italy, for example, a very recent investigation ended in April 2014 and conducted by the Prosecutor’s Office and the Finance Police of Palermo, has led to 17 individuals being arrested for taking unlawful public grants worth more than 15 million Euros (financed by the European Social Fund, ESF). An important Italian bank has engaged Be for an in-depth investigation of public funds fraud detection and prevention. Fraud against public funds actually may impact not only the public body itself but also other relevant organizations – mainly banks and other economic operators – who act as “outsourcers” of public funding provisioning services on behalf of Italian public bodies (e.g. the MISE, Ministry for Economic Development and the MIUR, Ministry for Research and Education). “Outsourcers” might appointed by the public bodies to oversee and/or coordinate a number of activities, e.g. the development and maintenance of the web portal to support the proposal submission and evaluation process, project evaluation, review and activity progress monitoring, the payment and monitoring of all economical aspects of the project (including on-site visits and audits). Main objective of the project was the assessment of the bank’s processes, practices and tools (including IT systems) in terms of appropriateness for the detection and prevention of frauds events. The final output has been the identification of action items to improve the current processes, and specifically to develop tools enabling the early detection of frauds and reduce their potential impact. The overall project approach has been organized into two main phases:

Project phases, methodology and deliverables In this project, Be carried out an in-depth analysis of the bank services and activities in the light of the potential happening of fraud and irregularities on public funds. The main goal of the project was to identify potential gaps in the bank’s processes and practices that could lead to frauds, and the design of appropriate detection tools in order to reduce fraud events and/or enable an early warning. To reach this goal Be has designed an ad hoc methodology for the definition of prevention tools and – whenever possible – of countermeasures that could strengthen the organizational and business structure against that occurrence of frauds. During the final phase of the project, we tailored an “ad hoc” tool (mainly in the form of KPI) to support the Risk Management in the discovery, early warning and prevention of fraud events. Analysis model for risk factor, loss events and loss impact The project started with an in depth assessment on a large sample of funding programs and the related “fraud prevention process” with a specific focus on the adequateness of internal controls and the presence of specific vulnerabilities that might favour frauds. Each risk factor was evaluated and associated with specific loss events, and related loss impact: loss events and related loss impact have been identified and characterized on the basis of the bank business activities, organizational framework, former fraud events, and other aspects which were considered as relevant. The analysis was conducted through extensive evaluation of the available documentation on national funds provisioning. A number of follow-up interviews with the key stakeholders (e.g. responsible for overseeing grant beneficiaries and/or responsible for grant project administration) were conducted as well, in order to tune and contextualize the arriving from the documentation. The investigation also included the analysis of specific case studies (selected in agreement with the Internal Audit itself) in order to realize a comprehensive investigation of activities that are/will be crucial for the business in the future. In parallel, best practices (from other similar Italian and/or EU institutions or programs) were selected in order to define recommendations, guidelines and practical countermeasures to proactively prevent fraud throughout the overall grants lifecycle. Common fraud schemes (by entity and program type) have been also identified and characterized using scenario/event based descriptions. The analysis also contributed to the definition of “red flags” and alerts for decision makers/operators in the case of fraud occurrence and the development of action items (short and long term) also including “quick wins” to improve fraud monitoring and detection, and start up the actual implementation of fraud prevention and detection techniques. | IT & Operating Model |

| 505 | How To Derive Value From “Artificial Adaptive Systems” | The fraudulent behaviors in the Telecommunications market are traditionally very complex to a point where they look turbulent in their continuous development and extremely high variability, which is due to the rapid technological evolution. All of this requires the Telecom companies to invest substantially in anti-fraud research and innovation processes, as well as to suffer high running costs for the maintenance of appropriate security standards. The usual technologies which are currently utilized to address and prevent credit and fraud risks have significant limitations both in relation to costs and their vulnerability. For this reason, Be has developed new innovative technologies based on quantitative methods, which are able to continuously learn from the observed behavior and, consequently, to rapidly adapt to the evolution of the “attack patterns” . In addition, the variety of Be services also includes best-of-breed technologies which allow our clients to innovate their internal processes at a very competitive cost. This month Be is finalizing a first pilot of “Artificial Adaptive Systems” for one of the leading Italian Telecom operators, which will lead to a second experimental project for next 6 months. The tactical goal of this project is to automate part of the manual work, based on the experience of experts in assessing the consistency of the information provided at the time of underwriting a new customer. The strategic goal is to fully exploit the potential of our tools in the preliminary assessment of “client risk”, through a joint analysis of company data available from CRM and other systems, and information provided by the client himself in the underwriting phase. The use of our technologies is meant to support analysts in developing highly specialized professional skills in anti-fraud detection, as it will allow them to focus on the most critical and valuable fraud instances. This will result in both an anti-fraud performance improvement (in terms of effectiveness of results) and a significant saving coming from more efficient organizational processes. | IT & Operating Model |

| 507 | The New Era Of Credit Risk And Liquidity Management | The craft of “good banking” is a fine art that has evolved over the centuries. It has always been based on a balance between profit, containment of credit risk and liquidity management. Credit risk is usually defined as the risk that a counterparty will not settle an obligation for full value. It stems out from the extension of any form of unsecured credit (i.e. non-collateralized) or/and from a failure in synchronizing the various interrelated elements (or “legs”) of a transaction. The above leads to an obvious – but not trivial – assumption: in finding the balance between pursuit of profit, containment of credit risk and liquidity management, collateral play a crucial role. They have been used for hundreds of years to provide securities against the possibility of payment default by the opposing party in a trade. In the 1980s, Bankers Trust and Salomon Brothers moved from simply “take” collateral to “manage collateral”. Collateral management includes a continuous process aimed to control the correspondence between the effective market value of the relevant collateral and their required value. At the very beginning, there were no legal standards and most calculations were performed manually. Collateralization of derivatives exposures became a widespread market practice in the early 1990s while standardization began in 1994 under pressure of IMF and Banking Associations. Collateral management has evolved rapidly in the last 15–20 years with increasing use of new technologies, competitive pressures in institutional finance, and heightened counterparty risk from the wide use of derivatives, securitization of asset pools, and leverage. The failure of Lehman Brothers on 15 September 2008 and the market stress that followed provided valuable insights into how market infrastructures and markets perform in very stressful conditions. Normally liquid markets become severely strained. The recent financial crisis has also exacerbated the relation between efficient management of collateral and its impact on capital adequacy needs of European banks. Under the pressure of the market discipline agreed by G20 to mitigate any new financial crises, retail and wholesale payment systems will evolve and unsecured interbank deposit markets will be gradually replaced by guaranteed ones. As a consequence, the use of collateral as a means for a balance between profit, risk containment and optimal management of liquidity has returned to play a central role in the art of banking. However, as collateral becomes scarcer it will also become an increasingly precious resource: on one hand, the level of collateral required for regulatory purposes will increase significantly; on the other, the current way of managing collateral shows significant inefficiencies estimated at about € 4 billion per year (source: Collateral Management – Unlocking the Potential in Collateral, Clearstream, 2011). The “next gen” in collateral management practices is represented by optimized use of collateral (substitution, re-use, etc.), a very complex process with interrelated functions involving multiple parties within banking organizations. | Insights, Risk & Compliance, Transaction Banking & Securities |

| 513 | Is GRC Just Another Acronym Or A Real Opportunity? | We all know that, in response to the recent financial crisis, regulators across the globe are focusing on a more robust supervision of all players in the financial services industry. A key effect of this trend is not only the launch of an increasing number of regulatory initiatives but also the fact that the Compliance function will become increasingly important in the near future. In February 2011, one of our major clients launched a project aimed at reinforcing, mapping and harmonising the so-called “second level controls” throughout the Group, on the key regulatory areas that fall under the Compliance function remit; as a result of this initiative, our client’s Global Compliance Framework went into effect in June 2011. In addition, in May 2012, their IT Department launched a project aimed at providing the whole Group with a new platform to be able to manage all three levels of controls (from Internal Controls to Internal Audit through Compliance) on a single system. This platform is based on a market standard solution widely used in the Governance Risk and Compliance space. The Open Compliance and Ethics Group (OCEG) defines GRC as a “system of people, processes and technology that enable an organization to”:

The basic building blocks of a GRC application include:

Return on Investment Although it is difficult to quantify the value added of a “global initiative”, fines and censure can highlight the potential cost of non-compliance;In any case some metrics have been developed to help calculate the potential value (see picture). Interaction with the “baseline” Regulatory risk assessment should be undertaken by each business line but responsibility ultimately lies with Compliance, which must perform the appropriate level of oversight and challenge. Under this framework, the business line would be able to apply its knowledge to assess the regulatory risks to which it is exposed. Compliance would then oversee this process in order to challenge the business on the identified risks. | Insights, Risk & Compliance |

| 516 | Video Banking Can Provide An Answer To The Request For Increased Productivity | People prefer to interact and learn visually. Our perception of what makes a good experience is influenced by the context of interactions and the interplay between our senses. This is particularly important as customers increasingly desire (and often do) control the time, place, channel and form in which they receive information. To date communication technology could not fully translate these communication types involved in face-to-face, therefore a targeted approach to the use of video is critical. A study of large European and North American banks and insurance companies found that 80% provided some form of video, either on their own site or on syndicated platforms such as YouTube, but very few have already started to interact with customers for retail banking, commercial or business banking. The recent developments in the field of digital video and communications technologies, such has interactive kiosks, have opened full breadth of opportunities to create valued experiences and improve productivity. This can be achieved using several technology experience concepts:

Be IT specialists can provide full project skills and experience in order to define the appropriate interactive model and implement video collaboration capability services throughout the bank. | IT & Operating Model |

| 518 | Paperless Operations, What’s The Real Challenge? | As most industry analysts have noted, the financial services industry is starting to embrace multiple aspects of a paperless transformation. The benefits stretch beyond mitigating risk, eliminating costs and improving operational efficiencies and move toward ultimately improving the customer and employee experience. A strong unrevealed amount of digital data will also be available to marketing/risk managers to improve bank’s understanding of costumers behavior. Individual approaches on paperless vary tremendously though. Some banks are slightly along the path and have implemented first electronic solutions, while others are just beginning to develop their strategies. Most fall somewhere in the middle still facing a long journey before they can reap the full benefits of an electronic environment and establishing a clear paperless operations acting at the core inner heart of the bank: the back office and the operations departments. A full paperless workflow would need 6 key elements in place to really take off in the bank organization:

Within this blueprint banks still need to do a lot. Be’s client teams at Unicredit and BNL-BNP Paribas are dedicated to help clients to manage this transformation. Be’s technology and operations are furthermore already in place to handle paperless back office processes as a service. | IT & Operating Model |

| 520 | RTO Emerges As A New Crucial Unit To Avoid Financial Disruption | The long-lasting financial crisis has generated a range of effects: the increasing competitive pressure, the difficulty to keep stable revenues streams, the lack of a trusted relationship with the consumer and corporate customers. Overall, we can say that today’s strong appetite of both global and domestic banks to avoid new “financial disruptions” has caused a deep re-focus of the industry priorities. Banks have now fully realized they need to redesign and reinforce the whole set of rules and tools devoted to control any form of risks. This is fairly easy to accept in relation to market and credit risks, as their potential impact is well known. But, and this is the real news, the “control framework” now needs to be extended to new risk areas, which had so far been considered as “lower priority”: the operational risk management. What is an RTO? In this context, banks are enriching their organizational structure with a new unit – the Retained Organization (RTO) – tasked to assure the appropriate level of control on those entities in charge of supporting the business: the outsourcers. The RTO remit is to guarantee that every service provider supporting the business operations, whether it is an external suppliers or an internal shared service center, complies in full to banking authorities requirements. How to structure an RTO? Two years ago, Be has been engaged by a leading European bank to manage a complex change program targeted at modeling and implementing the control framework for the main outsourcing providers. Our proposed approach was to use an “holistic” RTO design and implementation methodology, which includes:

Based on this methodology, our target was to complete the RTO set-up (with the exclusion of change management and IT implementation activities) within 5 months from start. Performance Management Model A key aspect is to define a consistent performance management model, to enable centralized monitoring of the providers’ business performance. We used a 3-step approach:

The level of reliability and consistency of the performance management model has a big impact on the effectiveness of the RTO. In particular, a well-designed model is likely to provide a very significant contribution to the bank’s overall business performance in terms of improvement of the customer service quality and identification of potential areas for efficiency gain and cost reduction. | Homepage, Insights, Risk & Compliance |

| 522 | Is “End-2-End” The New Paradigm In Performance Monitoring? | “End-2-End” is becoming a recurring definition to describe the new approaches utilised in the area of performance monitoring (and in banking, in general). When this definition is not misused, an “End-2-End” approach implies that one activity (eg. a specific business process) is monitored from only two observation points: the input and the output. No matter what happens in the middle! Applied to performance monitoring, “End-2-End” approaches produce the following implications: Service model and monitoring model Moving from a “service by nature” performance monitoring model to and “End-2-End” model implies a redefinition of final output accountability and forces a redefinition of KPIs, which evolve from being based on production factors (MIPS, FTEs, Function Points) to being based on business drivers (number of transactions); Processes: Processes can be more easily coupled with the business they are supporting; Market benchmarking: An “End-2-End” perspective allows an easier comparison of service quality and performance with external market players, without the constraints of considering the different infrastructure, applications and organisation utilized for service delivery; Compliance: An “End-2-End” perspective can potentially be unsatisfying for a Regulator, who requires each Bank to control its operating environment with an approach that allows to detect and understand in detail any cause of potential issue. This list of implications clearly provides an indication that any plan to switch to an “end-to-end” performance monitoring approach needs a preliminary “trade-off” evaluation between the expected value added and the “change” effort required. | Insights |

| 528 | Insurance Companies To Focus On Product Suitability | The UK has suffered several mis-selling scandals including Payment Protection Insurance (with billions paid in compensation) through to interest rate hedging products which appear to have been unsuitable for small businesses in 90% of cases investigated to-date. Little wonder the regulator is focused on improved customer outcomes. In the investment arena, we have just seen the first quarter since the implementation of the Retail Distribution Review and it seems that there have been two main changes: All of the retail banks have stopped providing advice via branch networks with advisory services only for those with £100,000 or more in investible assets Whilst independent adviser numbers are heading for a c15% reduction, this has been coupled to a move to restricted or tied advice – 8:10 biggest advice firms are now using the restricted model, marking a substantial swing from a pre-RDR independence ratio of 4:1 Fewer advisers and less choice are the unintended consequences of a drive for quality and a significant advice gap is now apparent. Life and pension providers, fund managers and discretionary fund managers have started to look at new direct to consumer (D2C) operations, following on from the start-up firms from 2010 onwards that have looked to tap self-directed consumers. All of the current solutions follow the same pattern, which is based on a stepped process to determine client suitability for a specific, but self-selected, product solution. This begins with the consumer determining a goal; quantifying a target amount and a timeframe. The user then tries to determine their risk appetite, typically via a questionnaire, followed by a check on risk capacity (the ability to sustain losses). The profile is then matched to a model portfolio which may be made up of ETFs, pre-packed funds or a fund of funds solution. The process is not really aimed at the novice investor and concepts of risk, return, volatility and even investment horizon do not speak to a client that is tentatively looking at better returns than they can get from cash deposits. The mass affluent is looking for a greater certainty of outcome and capital protection – outcomes that currently tend to come from complex structured products with accompanying credit risk. The result is that unless simplified products are designed, with better underwritten outcomes for the mass of consumers, there will be no uplift in consumer investment even with improved technologies and online education. Nor will the regulator be interested in dropping the bar on the regulation of the sales process until the consumer is better immunized against detriment from products and providers. This situation is not peculiar to the UK and authorities elsewhere have looked for suitable solutions. In the US, these have taken the form of “safe harbour” funds – protecting 401(k) plan sponsors from fiduciary liabilities and the UK tried once before with stakeholder products which were charge-capped. Government-backed simplified product design thinking is so far only extending to general insurance, income protection and savings products – with investments deemed too difficult, or inappropriate for the mass of consumers. But between below-inflation returns on savings and corporate pension schemes where members are bearing all the risk, the need for product-based solutions are clear and the firms that recognize this could capture a significant prize. | Life, Pensions & General Insurance |

| 530 | Pain With A Prospect Of Gain For European Insurers | European insurers seem to be trapped in a pincer movement between regulatory change and the potential impact from sovereign debt defaults and recession-driven declines on the asset values supporting insurers’ liabilities on the equity market. Low interest rates continue to impact financial resilience as life companies struggle to maintain margins and limit the impact on capital and reserves. We have already seen some insurers trying to increase product prices, some of it under the cover of changes in distribution regulation, but limited by weak consumer demand. In this tough environment, we can see some of the key responses from the main players:

In 2013, European insurers will increasingly focus on improving business retention and growth. Regulatory changes aimed at improving customer transparency about products and costs will sharpen this focus, guiding insurers to re-evaluate their business models and selling propositions. This is already seeing many insurers to alter their distribution, products and services — for example, shifting away from offering investment-linked options and emphasizing protection and customer service. In the UK, the implementation of the Retail Distribution Review has already been felt – leaving a significant regulated advice gap but a wave of new execution-only investment platforms. At the same time, Solvency II will pressure insurers to develop and market more products that shift risk to the insured and away from themselves and regulators have started to fear some consumer outcomes. For self-directed consumers, the internet has furthered their ability to compare products and prices and obtain independent opinions before purchasing, even if they use an advisor to complete the purchase. But time-poor and cash-poor consumers see the life insurance industry as lagging other sectors, especially with regard to service delivery and rewarding loyalty. Most life firms have been slow to react to social-media challenges and to harness consumer analytics as consumer data often resides in disparate product administration systems and formats or is constrained by intermediary relationships. So in 2013, European regulations will continue to have an important strategic and operational impact on insurers -MIFID II, PRIPs and the IMD proposals will all be on the agenda of the European Parliament this year. Although many details remain to be finalised and the necessary operational changes will vary by country, they will challenge existing distribution methods while creating opportunities to develop new models. In the meantime, firms look to cash flow control and product margin to get through the troubled times. | Life, Pensions & General Insurance |

| 532 | EU Launches New Short Selling Regulation | Since the 2008, amid the financial market turmoil, numerous countries imposed short selling bans to limit market bets on EU listed shares or bonds that caused falling in prizes, thus affecting market stability. From November, the new EU short selling regulation (236/2012) has come into force harmonizing provisions throughout the EU and soughting to regulate transactions outside its borders. It does not matter where a person entering into a short sale is located because this Regulation applies, broadly speaking, in respect of shares admitted to trading on EU trading venues, sovereign debt issued by EU sovereign issuers and related credit default swaps. In a nutshell, the key requirement are transparency in relation to short positions in shares or sovereign debt, restrictions on uncovered short sales in shares or sovereign debt or uncovered short positions in sovereign credit default swaps, buy-in procedures and strict monitoring on exemption for market making activities. In this contest, one the major Italian Bank Institution has launched in 2012 an extensive programme aimed to ensure both detective controls to ensure monitoring and compliance adherence to the Regulation, and in 2013 preventive controls to address and monitor trader´s activities as well. The nature of bank business involving large trading volumes, the coverage of 54 different countries and the gold plating role of local and EU regulators entails a significant level of complexity. Be, enhancing compliance expertise and capital markets practices, has been asked to provide continuous guidance among the different stakeholders, facing the scale of the international business model and risk mitigation needs, extending contribution from PMO to SME contributions. | Insights, Market & Investment Banking, Transaction Banking & Securities |

| 535 | Central Counterparty Clearing Reduces Market Risk | A Central Counterparty Clearing (CCP) interposes itself as legal counterparty to both sides of transactions in a market. Contracts are entered into bilaterally and then transferred by novation to the clearing house, which becomes the buyer to every seller and the seller to every buyer. CCPs have long been used by derivatives exchanges and a few securities exchanges and trading systems. In recent years CCPs have been introduced by many more security exchanges and have begun to provide their services to over-the-counter markets. A CCP has the potential to reduce significant risks to market participants, by imposing more robust risk control on all participants, by achieving multilateral netting of trades. A Central counterparty does not remove credit risk by itself from a market. If a market participant becomes insolvent its loss will still be borne by some or all its creditors in some manner. Instead a Central Counterparty redistributes counterparty risk replacing a firm’s exposure to bilateral credit risk (of variable quality) with the standard credit risk on the Central Counterparty. In order to reduce risk the CCPs adopts collateral policies and monitors the robustness of their clearing members and risks from the business that they are bringing to the CCP. This means collecting and analyzing information, from clearing members on large positions taken by their customers. A CCP also tends to enhance the liquidity of the markets that it serves, not only because it tends to reduce risks to participants but also because it facilitates anonymous trading. This can be attractive to firms that, for example, may not want to reveal that they are large buyers or sellers because they fear a market impact. The role of CCP is very important as a risk management failure has the potential to disrupt the markets that it serves. A Central Counterparty by definition concentrates and re-allocates risk. As such, it has the potential either to reduce or to increase the systemic risk in a market. As a consequence security regulators and central banks have a strong interest in CCP risk management. The CCP are de facto regulators and supervisors and impose financial discipline on the clearing members. In this scenario we are working with our client to support and help them to improve their operational processes and the interests of Front Office trading system implementing the rules concerning regulation of Over-the-Counter (OTC) derivatives markets as follows:

| Insights, Market & Investment Banking, Transaction Banking & Securities |

| 578 | post di bilanci e rel | prova | Blog |

| 696 | Loyalty Is Becoming The New Growth Enabler In Financial Services | Tesco, British Airways, Amex Membership Rewards, Millemiglia, Bonus Garanti, Sconti Banco-Posta, Nectar. We all know those loyalty programmes first as consumers and then as advisors of many of these market players. Since early 70’s, when manufacturers launched initiatives to stimulate their goods purchases (independent points collection), the loyalty initiatives have become the core of marketing planning for Retailers, Airlines, Fuel company (which launched the multiplayers collections and catalogues). By the end of 90’s Loyalty Programmes extended their application in the Utility and Banking industries. Loyalty became the crucial marketing tool (the 5th P of the Marketing Mix) when the mass market scenario changed in a “hypercompetitive” arena: consumers have been offered multiple choice, with an always growing number of players, higher penetration of products and a decreasing pricing curve. Brand loyalty has definitely lost its strength in keeping the relation with customers and the strategic marketing focus moved from customer acquisition to fight to maintain their monthly budget share. Different Loyalty initiatives offered all possible ways to drive profitable behaviors among customers, using any means possible: points, miles, rewards, incentives, enhancements, cashback. At Be we partner with some of the best-known global brands, helping them attract and retain customers by offering rewards for using their products. We develop loyalty solutions that are adaptable and flexible – tailored to the Partners’ specific needs. An effective Loyalty Programme can only be a customized one, based on:

As a Business Consultants firm we support our partner to identify the Best Option Loyalty Plan, independently of the technical solution. Paramount is to talk to each customer in the proper way and to avoid standardized rewards to all clients. Needless to say, we put all efforts driving innovation in the emerging digital and mobile spaces, the new innovative solution, with higher chance of success. Our aim is to align the loyalty to the business strategy ensuring a positive ROI. The virtuous circle we advocate to our Partner is based on:

| Cards & Loyalty, Homepage, Insights |

| 761 | How To Be Successful In Ambitious IT Transformation In Capital Markets | Increasing competitiveness in financial markets and the (“expected”) growth of both volume and complexity of financial instruments are bringing banks to enhance their technology platforms to ensure greater flexibility and be able to face challenges with an efficient time-to-market. More than two years ago, one of our clients, the Investment bank of a leading Italian banking Group, launched a challenging program in Italy to change their IT “skin” by implementing standardisation and better competitiveness in the investment banking business. The “New Architecture” program represented one of the most ambitious, challenging and large engagements ever launched in the IT Capital Markets environment to date in Italy, and definitely the biggest in the last few years, with over 70€ML budget in a 2-year timeline. The scope of the program was the complete IT architecture review, through the development of a new approach involving decoupling integration layers at all application levels, the adoption of the latest releases for core software suites (Golden Source, Mx3, Calypso) and the consequent changes to the operating models. With the main strategic objective of reducing the bank’s time-to-market through the improvement of the IT&OP Service Model, this immediately became the most important project for the bank itself and their large IT division. Project representatives were selected from all areas of the bank (IT, Operations, Business, Organization, Risk Management…), which created the need for a significant coordination effort delegated to our Be Consulting team. To give an idea of the complexity of such a wide program, one of the first challenges addressed was the definition of the program organizational workforce, with about 15-20 different Consulting and Integration companies and also 250 FTE on the field. Even logistics was an issue to address at that point! In addition, the bank found it very difficult to identify the Program Head, given the extensive mix of managerial and technical backgrounds involved in the project. On this engagement, today Be still covers the Program and Project Management role with activities distributed across four levels of the client’s organization structure: Program Head, Stream Leaders, critical sub-streams and support to functional teams on specific areas. Setting up a Be team (on average 15 FTE, with a peak of 22) with the appropriate level of expertise in both project management and investment banking products, as well as with significant vertical IT system knowledge, was key to satisfying the client’s high expectations. During August, while our office was closed for summer holiday, we were forced to ask our team for an additional effort, as an important project milestone had been postponed from July to mid-August. Internal and external resource availability became a critical problem for the Program Head, particularly if we consider the size of the impacted release. The whole project team worked incessantly for four weeks (including weekends!). We gave a fantastic example of client commitment, as we were the only consulting firm who was able to immediately guarantee the requested support during the holiday season, and provided a clear contribution to achieving the project goals. Thanks to this performance and trusted cooperation, Be has been able enlarge its presence at this client, by securing new contracts both in terms of project follow-ups and new engagements with this leading Italian bank. | Homepage, Market & Investment Banking |